AML Risk Assessment: Definition, Process, and Key Risks

To spot a money laundering threat before it becomes a problem is extremely important. If your business reputation gets tarnished with suspicion of a compliance breach, not only can you lose your customers’ trust, but you can also lose quite a big chunk of money. Since 2020, the US alone has levied approximately $27.9 billion in AML fines. So, the stakes are pretty high!

Anti-Money Laundering (AML) risk assessment can help you identify the places where your business is vulnerable to money laundering risks. When you know where the risks come from, and what the most urgent ones are, you can prioritize your resources and focus on eliminating the highest risks first. Let’s take a closer look at what the AML risk assessment is, explore regulatory expectations, business benefits, core risks, the assessment process, key indicators, and mistakes to avoid.

What is an AML Risk Assessment?

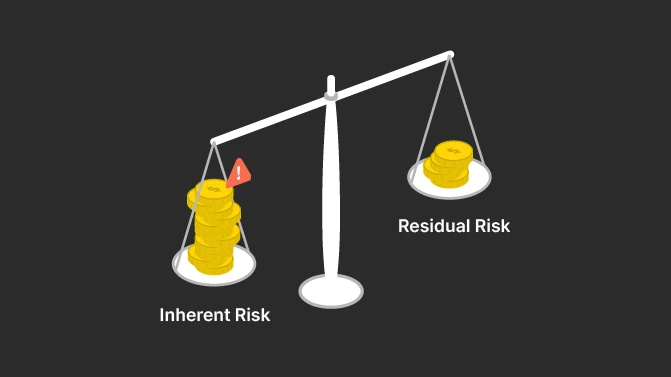

An AML risk assessment is a structured process of identifying, scoring, and documenting fraud or money laundering risks associated with customers, products, geographies, channels, and transactions. It helps differentiate inherent risk (the level of risk present if no controls existed) from residual risk (the risk remaining after mitigating measures are applied). These are the foundations of a strong AML program, its policies, processes and control mechanisms are built.

A well-documented AML risk assessment creates a clear map for your compliance teams to spot the biggest money laundering threats. In particular, it tells you which customers, products, and transactions deserve your closest scrutiny, and which ones can be monitored with lighter oversight. So, instead of spreading your efforts thin across everything, the AML risk assessment helps you work smarter by focusing on the areas that help your business grow.

Global Regulatory Expectations

First of all, an anti-money laundering risk assessment is a part of general compliance obligations. But rather than being a universal „one-size-fits-all” compliance method, this risk-based approach allows financial institutions to allocate resources where they are needed most – all with an aim to combat financial crime.

Global fines for anti-money laundering compliance failures jumped by 50% in 2022, and an estimated $2.7 trillion is laundered through the world economy each year.

Global regulators, such as the Financial Action Task Force (FATF), the European Union’s AML directives, and the US Financial Crimes Enforcement Network (FinCEN), require financial institutions and related businesses to conduct and document their AML risk assessments.

FATF:

- Sets global AML/CFT (counter-terrorist financing) standards.

- Requires countries and institutions to identify, assess, and understand money laundering and terrorist financing risks (Recommendation 1).

- The goal is to ensure that both regulators and businesses adopt a risk-based approach when designing their AML frameworks.

EU AML Directives:

- Make the risk-based approach mandatory across EU member states.

- Require firms to perform regular enterprise-wide AML risk assessments.

- These assessments should anticipate and address emerging threats, ensuring controls evolve with changing risks.

FinCEN:

- Expects all financial institutions to have a documented AML risk assessment as part of their compliance program.

- A recent rule proposal would explicitly require periodic AML/CFT risk assessments as a formal obligation.

- The US examiners treat a well-developed AML risk assessment as integral to a sound anti-money laundering compliance program – even if not always written directly into law.

To make sure organizations stay alert and effectively counteract the ever-evolving financial crime schemes, AML risk assessments have become important components of compliance audits and supervisory reviews. In short, well-documented AML programs are not optional – they are a regulatory expectation across global jurisdictions.

Business Importance

AML risk assessments are far from bureaucratic checkboxes. In fact, they are essential tools that help organizations address identified risks by:

Prioritizing limited compliance resources on the highest-risk areas.

- Allocate staff and budget to the areas of highest risk.

- Ensures high-risk customers, products, or geographies get enhanced monitoring, while low-risk ones are managed more efficiently.

Strengthening internal controls to prevent fraud and financial crime.

- Identify weak points (e.g., products or channels criminals might exploit) early.

- Improve due diligence, monitoring, and training to close gaps proactively.

Reducing the volume of false positives in transaction monitoring and inefficiency.

- Traditional monitoring systems can produce up to 95% false positives.

- Make your compliance teams spend less time chasing irrelevant alerts and more time investigating true risks.

Protecting the organization’s reputation by proactively managing risks before issues arise.

- Regulators and partners expect a documented AML risk assessment.

- A strong assessment demonstrates accountability, reassures stakeholders, and reduces reputational damage.

To sum up an AML risk assessment is a multi-functional management tool that protects your business, improves efficiency, and builds trust.

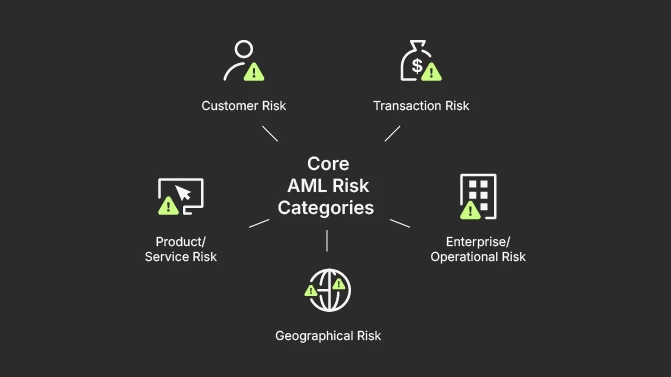

Core AML Risk Categories

AML risk assessments focus on several critical categories. Knowing the core AML risk categories helps you not to miss any major money laundering blind spots. By covering all the key areas, you can build defenses that actually work. Here are the core AML risk categories:

Customer Risk

Different customers may exhibit different financial crime risk levels. For example, if you do business with a cash-intensive business, like gambling, they will be inherently more prone to money laundering than a retail shop. The same logic applies to politically exposed persons (PEP) – they are higher risk due to their potential exposure to corruption.

More so, non-resident clients from high-risk jurisdictions or customers with complex company ownership structures also require enhanced scrutiny. Or a small business that suddenly displays an unusual volume of high-value transactions inconsistent with its industry norms is a red flag, triggering increased customer risk. Cases like these require Enhanced Due Diligence (EDD) and ongoing monitoring.

Product/Service Risk

Some products or services are inherently high risk. That’s why private banking, correspondent banking or trade finance services are often deemed higher risk because they can involve large, rapid movements of funds across borders. Also, newer products like cryptocurrency services, digital wallets, and prepaid cards are particularly susceptible to misuse given their relative anonymity and ease of cross-border transfers. For instance, a bank offering crypto custody services must implement robust controls reflective of the unique risks posed.

The assessment examines risk factors in each product line, like retail deposits vs. international wire transfers vs. insurance policies, and assigns risk ratings (low, medium, high) based on features like transaction limits, complexity, and financial crime typologies associated with that service.

Geographical Risk

Certain countries or geographic locations have higher money laundering risks due to weak regulations or corruption. That’s why it’s important to assess risks associated with specific countries or regions based on their regulatory landscape, political stability, and corruption levels. For example, countries on the FATF “grey list” or subject to sanctions or with high corruption scores are high-risk. Transactions linked to such countries automatically carry increased risk. So, if your client is engaged in frequent cross-border transfers to and from jurisdictions with weak AML regulations, they would trigger enhanced due diligence.

Channel Risk

Different onboarding and transaction channels have varying risk profiles. For example, non-face-to-face channels, like online onboarding or mobile banking, are of higher risk because it’s harder to verify identity remotely. For instance, an internet-only bank, considered high risk, will have to implement stringent digital identity checks and transaction monitoring tailored to virtual interactions. So, the AML channel risk assessment has to evaluate how customers access services and whether there’s additional vulnerability to illicit activity.

Transaction Risk

The nature, volume, complexity, and frequency of transactions could also signal suspicious patterns. Naturally, the unusual patterns are large, atypical cash deposits, rapid successive wire transfers – especially cross-border or to high-risk countries, rapid movement of funds through multiple accounts, or transactions noticeably inconsistent with a customer’s normal activity. All these behaviors may suggest money laundering attempts. For instance, a customer whose account is dormant but suddenly processes frequent high-value international wire transfers requires a deeper investigation.

Enterprise/Operational Risk

Beyond customer-facing risks, internal business risks play a critical role too. These risks are related to staffing competence, system capabilities, internal audits, and governance. For example, the adequacy of employee training, competency of the AML staff, effectiveness of the AML system capabilities, internal audits, and governance frameworks. A financial institution lacking sufficient AML expertise or using outdated technology is exposed to operational risk, potentially weakening its AML defenses.

AML Risk Assessment Process

Conducting an AML risk assessment involves a series of structured steps. Here is the typical process, broken into key steps or phases.

| AML risk assessment phase | Purpose | Example |

| Define scope and risk appetite | Set boundaries for the assessment and clarify how much risk the business is willing to accept. | A bank decides it will not accept customers from sanctioned countries. |

| Gather and clean data | Collect accurate information on customers, products, transactions, geographies, and channels. | Removing duplicate customer records before analyzing transaction volumes. |

| Identify & score inherent risks | Rate the natural (uncontrolled) risk levels across categories like customers, products, and geography. | 10% of customers are PEPs → scored as “high inherent customer risk.” |

| Evaluate effectiveness of existing controls | Evaluate how strong existing AML controls (CDD, EDD, monitoring, audits) are in practice. | Checking if sanctions screening catches 100% of blacklisted names. |

| Calculate residual risk | Determine the remaining risk after controls are applied. | Strong monitoring reduces “High” wire transfer risk to “Medium residual risk.” |

| Collect and report all results | Combines findings into reports, heat maps, or matrices for management and regulators. | A heat map shows non-resident customers in “red” (high risk), retail deposits in “green” (low). |

| Governance and board sign-off | Ensures senior management and the board review, approve, and own the results. | The board signs off that the company accepts moderate overall residual risk. |

Key AML Risk Indicators

Now we come to the point when we need to monitor the AML risk assessment processes that we have in place. To monitor AML risks over time, organizations track specific Key Risk Indicators (KRIs) that serve as early warning signals if risk levels are rising or controls are loosening up. Usually, KRIs are defined in order to quantify and report on the elements of the risk assessment. Here are examples of key KRIs:

- High-risk customer percentage rates how many of your customers are high-risk as compared to the total number of customers. If the percentage of risk profile customers is rising, it may mean that your business is taking on more risk, therefore an enhanced monitoring and due diligence should be applied. A related KRI could be the number of PEPs or other special high-risk clients onboarded.

- Alerts and case management metrics evaluate the health of your transaction monitoring and investigative processes. For example, you should keep an eye on the number of AML alerts generated in a certain period , and the percentage of alerts that escalate to a Suspicious Activity Report (SAR). A low SAR conversion rate might mean too many false positives. Your goal should always be to lower this number. Another critical indicator is the average time taken to close alerts or investigate security alerts. So, if they take too long to resolve, that’s a sign of strain that could lead to overlooked suspicious activities.

- Model performance and validation are important when evaluating the performance of your automated risk scoring or transaction monitoring tools. For example, your risk model needs “validation tests” to see if it catches what it’s supposed to. If too many errors show up, or if you haven’t updated it in a long time, that’s a red flag. This means that the model validation pass rate or the number of issues found in model validation exercises can indicate if your tools remain effective.

- KYC and CDD process indicators include things like the number of accounts with missing or outdated KYC information to make sure your customer information is accurate and up to date. A spike in lapsed KYC reviews means your understanding of those customers may be stale. Similarly, it’s advisable to track how many high-risk clients have had enhanced due diligence reviews completed on time.

Frequency and Triggers of AML Risks

A robust risk assessment framework involves regular checks: performed not only once a year as recommended, but also when certain circumstances require. A proactive approach is a great way to prevent risk assessment from becoming stale or missing emerging risks. The following situations may trigger additional assessment procedures:

Launch of new products or services

New products can introduce new risk factors. For example, if a bank starts offering a brand-new product (say, cryptocurrency trading), it should assess the money laundering risk of that new offering before the launch.

Expansion into new geographical markets

When entering a new geographical market, especially foreign, or targeting a new demographic are all triggers for risk assessment. For instance, when you start opening accounts for international clients.

Major incidents like regulatory sanctions or fraud cases

If your organization experiences a major compliance or SAR incident or a serious control failure, it’s wise to update the risk assessment to incorporate lessons learned. For example, if a large money laundering scheme was identified that exploited a certain product, the inherent risk of that product might be reassessed higher going forward.

Updates or changes in monitoring models or AML technology

If there are significant changes in laws or regulations, such as a new AML Act or a new sanctions list, this too calls for an ad hoc update of the AML risk assessment protocols. For example, if your regulator flags a control weakness (say in transaction monitoring calibration), your residual risk might increase until that’s fixed – and the assessment should note that.

Common Mistakes in the Risk Assessment Process

Implementing risk mitigation strategies can be challenging, and there are several common pitfalls to avoid. Here are some of the frequent mistakes that firms should be wary of:

First, it’s the mistake of using outdated or copy-paste templates without tailoring them to the organization’s specific risks. For example, a real estate agency used a generic AML risk assessment template designed for banks or other financial institutions. This oversight caused them to miss real estate-specific risks, such as suspicious cash purchases by shell companies, leading to gaps in compliance.

The second mistake is poor data quality or unclear data lineage which leads to inaccurate risk scores.

For example, a financial institution relied on inconsistent customer data with missing transaction histories. This can result in low-risk customers scoring as high risk and vice versa, skewing resource allocation and creating blind spots in risk management.

Next is the mistake of failing to validate or test AML models regularly. For instance, a bank deployed a transaction monitoring system but neglected regular model validation. Over time, changes in customer behavior rendered the model ineffective, producing excessive false positives and missing genuine suspicious activities.

The fourth mistake is to treat the assessment as a static, once-a-year activity rather than a dynamic, ongoing process. For instance, a wealth management firm completed a comprehensive AML risk assessment in January but failed to update it after launching cryptocurrency services mid-year. During this gap they were potentially exposed to new compliance risks.

Finally, be aware of scoring controls without proper evidence or testing, as this can give a false sense of security. Imagine an insurance company that claimed strong transaction monitoring controls without performing evidence-based testing. Internal audits later revealed controls were not functioning as expected, creating unintended risk exposure.

All these examples demonstrate how important it is to tailor risk assessments to your organization’s unique circumstances. To avoid common pitfalls in risk assessment and maintain a robust AML program, you need to ensure:

- data quality,

- ongoing model validation,

- frequent reassessment,

- objective control testing.

Industry-Specific Considerations

Even though each industry must comply with the same core anti-money laundering principles, money laundering risks can take different forms in different industries. That’s why AML risk assessments should also take into account the industry-specific context. Here are some examples of how risk assessment might differ for various types of institutions that deal with compliance, KYC, and CDD.

| Industry | Key risks | Example |

| Banking | Large customer base, multiple products, heavy regulators’ oversight, high-risk areas like correspondent banking. | A bank must monitor thousands of cross-border wires daily and each of them could hide illicit funds. |

| FinTech and payments | Fully digital onboarding, rapid scaling, third-party dependencies, serving higher-risk populations. | A digital wallet app suddenly doubles users in a month – can KYC checks keep up? |

| Crypto / VASPs | High inherent risk: anonymous transactions, fast cross-border flows, exposure to hacks and mixing services. | A crypto exchange sees funds routed through a mixer before hitting customer wallets. |

| Insurance | Products with cash value or quick withdrawals, agent/broker risk, overseas premium payments. | A customer buys a $500K life policy with cash, then cancels it early to “cash out clean”. |

| Gaming and gambling | Cash-heavy, VIP players, chip conversions, online betting channels, cross-border clientele. | A gambler buys chips with cash, plays a few rounds, and redeems them for a casino check. |

As you can see, the one-size approach won’t work across different business sectors.

Final thoughts

When done right, an AML risk assessment is a powerful tool that helps various businesses and organizations to employ compliance efforts intelligently and effectively. By understanding the definition, process, and key risks involved, and by avoiding common pitfalls, banks, FinTechs, insurers, crypto businesses, casinos, and others can build risk-based AML programs that not only satisfy regulators but actually catch and prevent illicit finance.

Today, everyone should be on alert as criminals are getting craftier and regulators are getting stricter. That’s why investing in a rock-solid AML risk assessment process is a secure business practice that can safeguard your organization’s integrity and help fight global financial crime.

FAQ